Are the good days of high FD rates about to come to an end?

The FD depositors have had a good time over the last one year. With the RBI having hiked repo rates by a total of 2.5% in the last 1+ year, the FD rates have also moved up significantly. And while many depositors have started putting in money in FDs of longer duration, there are still many who are confused what to do.

They are thinking that –

Is it a good time to book FDs at higher rates now than waiting more?

Let me offer you my view here (and not a recommendation).

Also, this view is for those who use bank Fixed Deposits (FDs) to park sufficiently large amounts. If you use debt funds instead of FDs as you understand the benefits (even after the change in debt fund taxation in 2023), then this article is not for you.

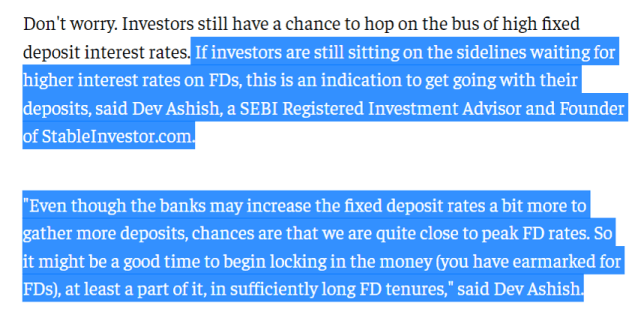

My views (in summary) were also published in The Economic Times (07-June-2023). You can read the full article using this link or have a look at my view quotes below:

Now let me elaborate on this view and try to share more detailed thoughts

Generally, the RBI Repo Rates are considered one of the major factors to assess the interest rate trajectory of the economy. And in the last year or so months, RBI has hiked repo rates (from a low of 4%) by a total of 2.5% to the current 6.50%.

While there are no guarantees, but given that RBI decided to not to change the policy repo rates in last 2 meetings in April and June 2023, there are now signs that if this is not the peak rate yet, even then the rates might be very close to peak rates (barring any unexpected or chaotic global event).

There is one thing to understand about FD rates and Repo rates. When the banks are deciding FD rates, the RBI Repo rate is not the only factor influencing the FD rates. The rates are also decided based on what is the credit demand growth and deposit growth rates, the bank’s own time-based asset-liability profile, overall liquidity, etc.

And please note that the banks are never in a hurry to pass on the full benefit of rate hikes to FD depositors (like they are in passing on the hikes to loan borrowers!).

But given all the factors at play now, the banks may still go for a little more increase in FD rates. But they may not as well. We can never be sure. And FD rates are pretty good enough now, at least for the common man who uses FD regularly.

Last year around this time (mid-2022), I had written that FD rates will go up to 7-8% soon. Here is the image from that article:

I had also said that FD rates may get quite close to 8% in 2023 (image below from the same article), which is now playing out

While there was nothing special about predicting this as simple factors were at play, the important question now is what to do now?

Should you start locking in FDs of Long Periods (for Several Years) Now?

I think Yes. Given that FD rates are near to their expected peaks this cycle, it is seemingly a good time to begin locking in the money (you have earmarked for FDs) in sufficiently long FD tenures like 3-5 years if not more. And if not all the money, then at least a major chunk. You will easily get 7-7.5% FD rates for long duration for most banks. The Small Finance Banks offer higher rates but you should limit your exposure to them if you have to make FDs with them

So historically speaking, these are already decent FD rates and its better to start locking in your money if you’re a FD person.

What if you still want to wait more for rate hikes?

Your money your decision. Up to you. You can rely on timing your deposit as close to highest FD rates that you can get. Or you can start now also. You can even go for FD laddering in 3 parts (just as an example). Say you have Rs 20 lakh that you want to put in a bank FD. Then consider deploying at least 70-75%, i.e., about Rs 14-15 lakh in 5+ year FD and lock-in the high rates over the next month or so. With rest, you can wait for higher rates if you want to do that.

And if you have a large amount (much higher than Rs 5 lakh DICGC Deposit Guarantee) to put in banks, then spread your FDs across a few banks. Put at least 65-80% in RBI-identified SIBs or Safest Banks of India. The rest you can park in other banks, which may seem attractive to you on the basis of higher interest rate offers.

And if you have old FDs that you booked a year or two back at much lower rates? Should you break Old FD to make new FD at higher rates?

Don’t be in a hurry to do that. If your FDs are close to maturity in a few months, then don’t go for premature withdrawal and lose interest and pay penalty. Let those FDs mature in due course as you may still get reasonably high FD rates in a few months’ time to lock-in for new FDs you make later. Go for premature FD closure only if there is a large gap between the new FD rates on offer and the old rates on your existing FDs and also, if a sufficiently long time is still left in the tenure of the old FD.

I would like to repeat here this article mainly focused on those who generally use bank Fixed Deposits (FDs) to park short-term money (for a few years). If you are comfortable with mutual funds and use debt funds instead of bank FDs as you understand the benefits, then this article is not for you.

Related Reading – Will debt fund returns improve in 2023-24?

Disclaimer – The views expressed above should not be considered professional investment advice or advertisement or otherwise. The article is for general educational purposes only. The readers are requested to take into consideration all the risk factors including their financial condition, suitability to risk-return profile and the likes and take professional investment advice before taking any financial decisions or actions which may have financial implications now or in future.

Yes.Some banks have started reducing FD rates.It is right time to consider booking FDs in good banks.